AI Is Disrupting the Analyst Industry. And That’s Good News (for Buyers).

AI fundamentally changes how marketers research, evaluate, and buy technology. This piece explores what that means for the analyst industry, and how CMOs should rethink their decision frameworks in an AI-first world.

For decades, the analyst industry played a central role in how technology gets bought. A CMO, CIO, or Head of Digital trying to navigate a complex martech or data stack, turned to firms like Gartner Group and Forrester. You paid for research. You booked inquiry calls. You waited for Magic Quadrants and Waves. You relied on vendor positioning to help reduce risk.

The old analyst business model worked when information was scarce. It no longer is.

AI has fundamentally changed the economics of research. It can summarize markets, compare platforms, analyze vendor claims, normalize feature matrices, and model TCO in seconds. Large analyst firms built their businesses on that informational advantage. For the most part, that advantage has effectively collapsed.

And the impact of that collapse is going to reverberate far and wide.

This doesn’t mean analysts are going away. It means the old analyst business model is.

The End of the Research Paywall

The core product of large analyst firms has always been information packaging:

- Market overviews

- Vendor comparisons

- Category definitions

- Trend reports

- Frameworks & Best practices

For decades, those lived behind expensive subscription paywalls. Buyers paid. Not because the research was extraordinary, but because there was no alternative.

Now there is.

AI can ingest earnings calls, product documentation, pricing models, security disclosures, roadmap statements, customer reviews, and even architectural diagrams and synthesize them rapidly.

In practice, however, this synthesis is often incomplete, uneven, and occasionally wrong. It is constrained by information scarcity, selective disclosure, inconsistent terminology, and the lack of primary validation that comes from direct vendor and customer interaction. That said, the implication remains the same.

For many buyers, the perceived sufficiency of AI-generated analysis now outweighs its actual accuracy. Feature matrices, competitive landscapes, and “good enough” comparisons can be produced faster, and often appear to be more current than analyst reports published months later, even if they lack depth, context, or reliability.

In other words, it isn’t that the quality of analyst research has been fully replicated by AI. It’s that the “what” layer of analyst research has been functionally commoditized in the eyes of many buyers who are increasingly comfortable trading precision and validation for speed, clarity, and narrative coherence.

The notion that buyers need to pay $80,000 a year for access to PDFs explaining what a CDP is, how composable architecture works, or what the difference is between batch and real-time marketing is increasingly hard to justify.

That part of the business is going to shrink.

The Structural Problem for Big Analyst Firms

Large analyst firms were built for a pre-AI world:

- When vendor information was fragmented

- When architectures were opaque

- When synthesis was slow and expensive

- When buyers needed guided education

AI reverses all of that. Much of analyst output today is already formulaic:

- Repackaged vendor briefings

- Sanitized market positioning

- Carefully worded commentary that offends no one

- Frameworks designed to preserve vendor relationships

- Research written to support reprint sales

AI is extremely good at that kind of work. Which means the middle of the analyst market “the research factory” is on the nomination list to be automated.

What will remain is brand, enterprise procurement contracts, and boardroom credibility. Gartner and Forrester will still be used as “checkbox” validators. Their logos will still appear in decks. Their quotes will still show up in vendor pitches. But their influence over buying decisions will decline.

Because buyers will no longer confuse access to information with judgment.

Where Boutique Analysts Win

As AI floods the market with information, buyers are realizing something important. Information isn’t what they need.

They need judgment.

They need context.

They need experience.

They need to know what really happens when a platform is implemented at scale. They need to know which vendors oversell. They need to know which roadmaps are fiction. They need to know who is quietly underinvesting in engineering and who is about to get acquired.

“AI can tell you what vendors say. Not who’s overselling.”

That is where boutique analyst firms live. Boutiques don’t sell research, instead they sell outcomes.

- They provide guidance in vendor selection and design sandboxes.

- They curate deep market intelligence, platform analysis, and practitioner perspectives.

- They operate as domain experts focused on specific disciplines such as retail, financial services, customer engagement, CDPs, or data platforms.

- They negotiate contracts.

- They fix failed implementations.

They live inside real transformations, instead of market categories. And because they aren’t structurally dependent on vendor sponsorships, they can afford to be honest.

For instance, they can say:

“Don’t buy this platform. It will fail.”

“This roadmap will slip.”

“This architecture will not scale.”

“This vendor is being shopped.”

That independence is priceless.

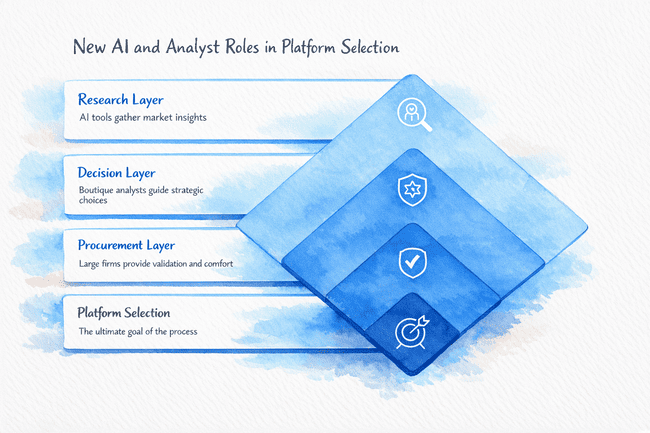

The New Analyst Stack

In this time of AI, the analyst model is being rewritten.

AI becomes the first layer of research:

- Market mapping

- Vendor discovery

- Feature comparisons

- Architecture education

Boutique analysts become the decision layer:

- Platform selection

- Commercial negotiation

- Implementation strategy

- Risk management

Large analyst firms become the procurement layer:

- Brand validation

- Boardroom comfort

- Risk signaling

The hierarchy flips. Instead of analysts being the gatekeepers of knowledge, they become translators of reality.

The Bottom Line

AI isn’t replacing all analysts. It’s replacing lazy analysis.

If your work is built on generic frameworks, surface-level research, or repackaged information, AI will get there faster and cheaper.

Insight still comes from judgment, context, and experience — not from access to more data.

What survives is real expertise, real experience, and real accountability. The future of the analyst industry belongs to people who have scars, opinions, and receipts. And that, frankly, is how it should be.